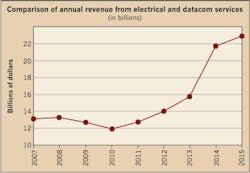

The nation’s largest electrical contractors booked record electrical and datacom revenues in 2015, further distancing themselves from the trough hit in 2010.

This year’s Top 50, as ranked by Electrical Construction & Maintenance (EC&M), EW’s sister publication, on the basis of a self-reporting survey (see List on page 18), collectively saw $22.8 billion in sales, just topping the $21.8 billion reported for 2014, but nearly doubling revenue reported during the depths of the turn-of-the-decade financial crisis (Fig. 1 on page 18).

The climb from the $11.9 billion in revenue tallied by the 2010 EC&M Top 50, following a period of fairly stable revenues, had been steady up until 2014. But after hitting $15.7 billion in 2013, reported billings surged 38% in 2014 to $21.8 billion, offering solid evidence that the construction economy had gotten back on its feet, and then some.

The question now is whether growth is peaking or merely catching its breath before another push upward. With the durable but tepid economic recovery well into its seventh year and a possible inflection point looming on the course of interest rates, further economic stimulus, and the trajectory of the financial markets, the smart money might be on a pullback. However, more buzz about the prospects for increased stimulative national infrastructure spending could keep the broader construction economy humming.

All of that is out of electrical contractors’ hands, but what is under their control is how they position themselves for the future. And on that score, this year’s Top 50, 61% of whom characterized 2015 as business-friendly, exhibit a blend of tempered optimism, eagerness to explore emerging opportunities, and caution in how they approach the marketplace.

“We have a lot of work on the books for this year, and there doesn’t seem to be a shortage of opportunities to bid,” says Russ Lancey, vice president of Five Star Electric Corp. (No. 10), Ozone Park, N.Y. “But, by choice, we’re trying to be more selective, and rather than just seeking the bigger jobs, we’re looking to increase profitability where we can allocate our resources more effectively.”

Five Star’s 2015 revenue growth of 1.1% was slightly above that of the 2016 Top 50 collectively, whose ranks include six companies that did not crack the 2015 list and a top 15 that basically retained their positions. Among that unchanged top one-third or so, the highest revenue gainer reported a 24% boost, while the worst experienced a 14% revenue decline. Only three of the top 15 reported declines.

Five Star was among the 41% saying they met their revenue goals for 2015. Following a year in which industry revenues ballooned but still met the expectations of 55% of last year’s Top 50, it seems many anticipated the 2014 growth but were not expecting the party to last into 2015. As it turned out, many ended up pleasantly surprised even though industry revenue growth effectively stalled — 45% said company revenues exceeded their goals, compared with 31% the year before.

Revenues surprised Alterman Inc., (No. 43), San Antonio, Texas. Absent from last year’s Top 50, Alterman’s sales inflated as some jobs ramped up earlier than expected, and a division acquired earlier in Austin began hitting its stride.

“Last year, we had opportunities that ended up stretching us a bit, including two data center projects that came up that no one else in the market could really handle,” says President and CEO John Wright. “We also had to pass on some opportunities because our resources were stretched to the max.”

At Power Design, Inc., (No. 22), St. Petersburg, Fla., billings surged almost 11%, surpassing projections, says Lauren Permuy, vice president of business development. A robust multi-family housing market, the company’s niche, helped it enjoy its best year ever.

“We saw more large-scale projects in our big south Florida market, and we also broke into the California market for the first time with three big projects,” Permuy says. “On top of that, in the wake of a large competitor going out of business in 2014, there was a flight to quality (quality contractors that could be trusted) by customers, and we ended up getting some of that work.”

While 2015 may justify optimism, it’s not overwhelming for 2016. Mirroring last year’s results, this year’s crop of top contractors split almost evenly between projecting sales on target and exceeding expectations. Forty-six percent think sales will come in higher while 48% think no big upside surprise is in the cards.

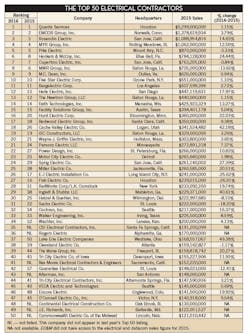

More telling, perhaps, are the hard numbers contractors attach to their growth prospects. In the wake of a year that saw revenue growth flatten, preceded by one in which growth was off the charts, the exercise of projecting final sales numbers is academic. More, however, seem to be taking their cue from what happened to overall industry revenue in 2015. Thus, in this year’s survey results, there’s a little stronger whiff of pessimism. A third of the group saw revenue declines. For instance, while nine respondents projected company revenue declines heading into last year, 13 did so in this year’s survey looking ahead to 2016. The biggest shift: Seven predict falloffs of 5% or less, compared with two the prior year (Fig. 2).

Still, projections of revenue growth again outnumber those for declines, and slightly more respondents in this year’s survey see revenues for their companies growing, though many have more tempered forecasts. Twenty-nine respondents see a revenue increase in the cards; in the prior survey, 27 foresaw an increase. The bigger discrepancy is in the numbers predicting growth of more than 10%. Whereas 15 of the 2015 Top 50 saw that for last year, only eight of this year’s leading firms see top-line numbers coming in that strong.

Managing growth. While long-term growth is essential, many contractors may be taking a more nuanced view of it. Not all growth is good, some suggest, emphasizing the importance of deliberate, controlled, and selective expansion that leads to higher receipts and positioning for the future. That’s playing out at Cupertino Electric, Inc., (No. 7), San Jose, Calif., where opportunities are coming at a faster clip. Coming off a year when revenue grew less than 1%, the company doesn’t feel especially pressured to pick up the pace or volume of billings. The emphasis instead, says President and CEO John Boncher, is on sifting through prospects to find jobs that offer more predictability.

“A lot of projects on the surface can look like fantastic opportunities, but when you look at the variables, they turn out to be not fantastic but wildly risky,” Boncher says. “We think now is the time to be very cautious, understanding in detail the makeup of project teams, schedules, partners and the like.”

Cupertino has begun applying more of that scrutiny to data center projects especially. A key revenue source for the company, IT project opportunities continue to beckon, Boncher says. But an increasing number of them are structured to require flawless execution on the part of too many untested parties. That’s a risk he’s less willing to take.

“We’ve decided to focus on a handful of data center customers who think differently,” he says. “We’ll probably end up building more square feet of data center space, but do so with far fewer customers.”

Likewise, CSI Electrical Contractors (No. 35), Santa Fe Springs, Calif., envisions being more selective in how it books more business. Coming off a year that saw billings climb around 35% as solar PV projects bunched up, the company will try to catch its breath in 2016 as it sees the growth rate coming down to around 10%, says Paul Pica, president and COO.

“We could get caught up in a frenzy for more work, but we’ll probably take it slower and be less aggressive in the pursuit of projects and more selective in finding jobs where can do good work for the customer,” Pica says.

Lingering concerns about the sustainability of growth in the Texas economy has Alterman scaling back its forecasts for revenue growth. After a big 2015, Wright thinks there’s a good chance it could stall in 2016 as fewer large construction projects are put out for bid. To stay on a growth trajectory, the company will look to new construction services markets like water/wastewater and other industrial work, and use the special projects capabilities in its growing Austin division to seize more building services and voice/data/security/AV opportunities.

“Geographical diversification via the office in Austin, where there’s less competition, is our way of dealing with concerns about the economy,” says Wright.

Strategic market positioning is another way contractors are navigating what could prove to be a frothy construction economy. Overwhelmingly, generalists working in the general building market (commercial/institutional/health care/housing) in this year’s Top 50 includes many trying to spot emerging sectors and nimbly acquiring the expertise needed to tap new markets.

That only grows more important as new opportunities sprout, tired sectors fade, and markets cycle. Contractors working in markets related to the depressed energy economy, for instance, have suffered, while those working in sectors sensitive to demographic changes, rising demand, and technological advancements have flourished.

For the second survey in a row, more contractors named health care and data center/mission critical as sectors generating the largest volume of projects for their firms. Power (utilities/T&D) and private office also ranked high. Troubles in the mining industry hit Minneapolis-based Parsons Electric LLC (No. 21) hard last year, but the company continued to unearth new business in its growing technologies division. President Joel Moryn says the company installed sound systems for several new NFL team stadiums — a fresh challenge that might lead to ongoing opportunities.

“Those types of projects complement our standard electrical contracting work, and that sound/broadcast/Wi-Fi systems work is pretty steady and recession proof,” he says. “It’s a small niche that has only a couple of national players.”

As it refines its approach to the robust data center market, Cupertino Electric is also looking to develop other markets. Two are utility-scale solar and private office construction, the latter fueled partly by high-tech company interest in signature-scale headquarters projects.

“Campus high-rise projects are booming, and that’s also driving a need for energy-efficient, smart buildings,” Boncher says.

Behind health care and data center/mission critical, private office garnered the third-most mentions among sectors likely to deliver the most projects in 2016. As those office projects grow more sophisticated, the role of electrical contractors is almost certain to expand.

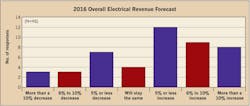

Incorporating energy management, automation and control, and submetering systems, next-generation commercial buildings will require increasingly complex electrical infrastructures. For the near future, though, contractors see a slow pace of adoption of some of the more sophisticated features. Of several different broad commercial building projects that are emerging, contractors overwhelmingly identified lighting and control systems as the source of more revenues (Fig. 3).

Over time, lighting solutions that vendors and contractors deliver could grow to be more all-encompassing. Under such a “Lighting as a Service” (LaaS) model, suppliers would move beyond a one-time installation scenario to one in which energy management, regular replacement, maintenance, and upgrades would be offered on a quasi-subscription basis.

Contractor views on LaaS are mixed, however. About a quarter of survey respondents labeled it mere “hype,” and only a half-dozen said they were actively marketing it to customers. Yet most agreed it’s actually compelling and something they’ll pursue as it takes root (Fig. 4).

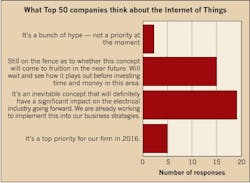

Likewise, a majority of contractors surveyed have an optimistic if not clear-eyed view of how the embryonic Internet of Things (IoT) might impact them. The IoT and Industrial Internet of Things (IIoT) hold the promise of taking building and industrial automation and control to new heights through advanced sensoring and communication. Half of those who weighed in on it agreed its eventual emergence was “inevitable,” and that it’s already being factored into their business strategies at some level (Fig. 5 on page 22).

Private office is seen as a new top revenue generator for Continental Electrical Construction (No. 48), Oak Brook, Ill. But low-voltage work has grown to account for about 20% of revenues, says Vice President Steve Witz. Alongside that, it does work in the data center and health care market, and is also looking to crack new markets.

“We’re making an effort to go after industrial work and bid more municipal projects, such as the O’Hare International Airport expansion,” he says. “Another new trend is the ‘green’ market, where we’re landing some solar battery storage projects.”

The profit picture. Keeping the project pipeline full and the cash flowing are primary concerns of labor-intensive contractors, but profits are certainly no less of a worry. As always, contractors were scouring for opportunities to build more profit into jobs in 2015 and are again in 2016. However, there’s evidence that more may be concluding and that appreciable margin expansions may be unattainable in the current market.

Heading into 2015, 43% of last year’s Top 50 contractors, perhaps anticipating the robust demand that did materialize, said they were planning to work higher profits into their bids. But data from this year’s survey suggests many didn’t succeed in extracting higher profits from their work. Just 23% of respondents said they were able to make bid adjustments that resulted in improved margins. And that was down from 33% of the 2015 Top 50 who said they were generally able to successfully factor more profit into their proposals in 2014.

Increasing margin pressure is a leading concern of Cupertino Electric’s top executive, and it helps explain why the company is being more careful in bidding jobs. Despite a climate where work is plentiful and demand is exceeding supply, which should be fuel for higher profits, Boncher instead sees aggressive bidding and an extreme low-bid award mind-set by buyers.

“Unlike previous expansions, like we saw in the dotcom boom when prices floated up as demand increased, pricing doesn’t seem to be moving up at the pace it should,” he says.

Boncher says he’s grown more wary of partnering with contractors who’ve won highly contested jobs, fearing they’ve cut corners and priced them for a perfect delivery scenario. That leaves too much exposure on reworks for which there’s too little padding.

“Big, giant hard-bid projects are not something we’re interested in now, because you have no idea who’s on your team,” he says. “All you know is that they were the low guy.”

However, jobs that are challenging — even to the point of being unreasonable — may be the ticket to higher margins in this market, says Continental Electrical Construction’s Witz. Coming off a year in which revenues grew smartly but profit targets weren’t hit, Witz is eager to find more lucrative work and thinks it lies in the more demanding recesses of the market.

“We’re into fast-track, tightly scheduled jobs that require large amounts of manpower and are considered specialty or mission critical — places where the ordinary Joe can’t get it done,” he says.

Profits are being squeezed, he adds, partly by contractors who still have the mentality of winning work at any cost, a holdover from the lean years experienced in the early decade.

For Encore Electric, Inc., (No. 46), Englewood, Colo., one route to higher profits may lie in playing to its strengths handling complex work, while steering clear of commodity-type jobs. The latter is abundant in the company’s market in the form of multi-family construction and the like, says Business Development Chief Chris Cole, but so is work involving mission-critical research, aerospace, health care and biomedical applications.

“Those are the types of projects that allow us to differentiate ourselves and win on qualifications, teamwork, and commitment,” he says. “That will help us achieve benefits for the bottom line of the business.”

Not all contractors are so positioned, so the drive for sustained profit growth could be an uphill battle. Top 50 survey respondents seem to recognize that; 68% say they’ll play it safe and not make bid adjustments for more profit this year, up from 57% a year ago.

Managing costs. Another route to higher profits is better cost control. But a big component of outlays is labor, an area the survey suggests is a concern for many contractors. The results point to a tight labor market, difficulty filling key positions, and the cycling in of less skilled and experienced people, all of which frustrate efforts to contain costs.

Contractors may also be facing a new set of challenges to the bottom line in the form of labor-related regulatory compliance. In the process of digesting stepped up government enforcement of workplace safety regulations that took effect early this year, more contractors say they’re chiefly concerned about what it will take to comply with the new OSHA rules on electronic recordkeeping.

Regardless of their impact, contractor labor force additions are on the rise, and that’s almost certainly a function of growing volume. Seventy-six percent of top contractors said they added employees in 2015, up from 69% the prior year. And additions appeared to exceed expectations because 70% last year said they expected to add to their 2015 payrolls. That’s the same percentage that expect to add to their payrolls in 2016.

After ramping up its workforce to handle a flood of work last year, CSI will likely ratchet back hiring in 2016. Nevertheless, COO Pica says he’s in a perpetual hiring mind-set because qualified workers that can work more efficiently are at a premium.

“All kinds of talent is harder to find, but the main concern is skilled craftspeople,” he says. “Like other contractors, we’re trying to find the quantities we need to support larger projects, and the first ones to the well will get the people.”

Power Design continues to add employees as it expands its geographic reach, but it sees improved employee retention as a way to combat the cost drain of scaling up and down on hiring. Permuy says the company is focused on training and support to keep the workforce intact. To cut down on labor costs, it’s turning to more prefabrication.

“By getting materials that are plug-and-play, what used to take three or four guys to do can take one or two,” she says.

That can be an especially important consideration when workers are simply harder to find, a reality in today’s construction market. This year’s survey again finds almost three-quarters of contractors frustrated by the challenge of worker shortages. Just 27% said they weren’t facing labor shortage “issues,” a sign perhaps that worries are commonplace and confounding for contractors.

This is supported by the finding — echoing the 2015 survey — that shortages extend into the ranks of the more broadly skilled and highly trained. Job superintendent, foreman and estimator — jobs that carry significant responsibility for project success — were identified most often as the hardest to fill. According to Boncher, Cupertino Electric is increasingly challenged to fill those and other critical jobs, especially as seasoned professionals retire at a faster pace. That’s particularly worrisome as projects grow more complex and demanding.

“Baby Boomers retiring is a big concern, because they know what it takes to get these projects built,” he says. “There are very smart, energetic younger people coming up, but they don’t have years of experience. So we’re seeing more projects built by those doing it for the very first time.”

Labor shortages are also the product of an exodus of skilled construction following the last recession. Parsons, Moryn says, is pressured to fill more skilled field leadership roles as project volume is pursued to make up for losses of big-ticket jobs in the struggling mining sector.

“A lot of people left for other careers, and trade schools have been decimated,” he says. “We have to be able to demonstrate through better outreach that our industry is exciting and interesting.”

Technology’s impact. The industry’s growing orientation to technology — applied in how projects are designed and bid, what’s being built, and even how work gets done on the job site — should help the electrical contracting industry to make its case to young, tech-savvy talent skeptical of the industry’s “cool” factor.

One small but telling piece of evidence is contractors’ strong embrace of mobile IT. Not a single contractor said its field workforce wasn’t routinely reliant on a mobile device on the job site. In conjunction with software and apps, the devices, contractors say, are fast becoming an essential tool for timely communication, collaboration, and coordination, potentially improving productivity and accuracy (Fig. 6 and Fig. 7).

Coinciding with the labor challenge contractors are facing, the proliferation of more powerful and user-friendly devices — notably smartphones and tablets — may be helping contractors blunt that impact. At the same time, however, contractors are striving to ensure workers use mobile technology responsibly and safely; nearly all say they have usage guidelines in place.

At their most useful, mobile devices help contractors work more in real time. Design changes, for example, can be more readily shared and communicated, as can exact conditions on the ground. With the ability to bring in multiple parties to view images from the field, reference diagrams, and consult calculation apps, mobile-equipped personnel can execute more quickly and accurately.

As Alterman’s use of more powerful design and modeling software ramped up, it reached a point where the communications component was hindering its value. Now, says CEO Wright, with foremen and higher types carrying smartphones and iPads, the value of those computing resources has greatly expanded.

“Four years ago, we started pushing out of our comfort zone on this, realizing that the technology had gotten better, but communication was lacking,” he says. “More instantaneous communication was needed in getting plan changes out to the field. Now, when an owner wants to change where a light is, for instance, it can be communicated instantly.”

At Power Design, all job supervisors and foremen work from iPads, Permuy says, ensuring they have ready access to an array of digital resources.

“Drawings and markups can be shared in real time, as well as programs we’ve created internally that detail different installation techniques,” she says.

In a business where time is money — to the extreme — the growing penetration of mobile devices may be a metaphor for the impact technology as a whole is exerting on productivity and project execution in the contracting world. As this latest survey demonstrates, as long as things continue to be built, business will keep coming for electrical contractors. But to rise to upper echelons of a growing and increasingly demanding industry, contractors will have to smartly leverage not only technology, but also people. They’re fast being confirmed as the sturdy pillars of successful and growing electrical contracting companies in an increasingly competitive but opportunity-rich industry.

Zind is a freelance writer based in Lee’s Summit, Mo. He can be reached at [email protected].