Let me share with you what we are teaching at graduate school these days. From the 1980s until recently, we talked about being in the Consumer Era, and how manufacturers wouldn’t make anything until they asked the consumer what they wanted. This strategy took all the pressure off sales and cut down obsolete stock on the inventory management front.

Then Steve Jobs came along with his disruptive vision that we are in the Innovation Era, and that you can ask the consumers all day long what they want, and they just do not know what they want, or what is even possible. To succeed in this era, best-in-class high-tech companies now must do the following:

1. Innovate like crazy. Best-in-class companies utilize a strategy of “discontinuous innovation,” and apply a new technology to solve an existing need in a new way. To do this yourself, create an environment within your company to think exponentially and develop the most innovate product commercially feasible. Discontinuous innovations “cause a paradigm shift in science or technology and/or the market structure of an industry,” according to the Financial Times.

2. Do post-purchase evaluations. Ask the Innovators and Early Adopters what they liked about the product, what they didn’t like, what they would like to see added, etc. (see chart on page 20).

3. Innovate some more. Continuous innovation will get you to the Early and Late Majorities that are absolutely necessary for success.

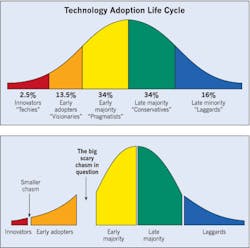

Now let’s talk about the Technology Adoption Life Cycle (TALC). As the chart at the top of page 20 indicates, approximately 16% percent of the market will try anything that even suggests high-tech. These customers are the Techies and Visionaries. They are the folks who sleep overnight on the street in Times Square to get the new iPhone. They pursue new high technology products aggressively. They love anything new, anything high-tech, anything that allows them to be first with the newest.

Today, this 16% of the market is big, full of enthusiasm and vision, and they are the most knowledgeable. They do know what they want and what they like. So ask them. Winning them over is essential if you want to reach the next group, the 68% that makes up the bulk of the market. Be guided accordingly. The Techies and Visionaries are key to opening up any high-tech market segment.

I’m reading a book titled Crossing the Chasm by Geoffrey A. Moore that focuses on marketing and selling disruptive products to mainstream customers. His premise is that a chasm exists between the 16% early market and the mainstream 68% majority markets — a chasm between being first with new technology to the majorities that are more practical and want assurances that the product becomes an established standard and is supported effectively. Each group represents a unique psychographic profile.

Bridging the Gap in Lighting

So what does all of this have to do with lighting? In my debate with Chris Brown, I contend that we are in a transition. A possible chasm exists between the traditional lighting business and the developing intelligent solid-state lighting (SSL) business. I believe we have crossed the chasm. In the high-tech innovation era, the process is to move smoothly through the TALC, maintaining the momentum to make it natural for the next group to want to buy in, even the laggards. In the lighting industry, we are moving through the TALC faster than at any time in our history.

But what about the service side? Who will satisfy the growing need for the service demand that is always present when it comes to electronics? I believe it will be the channels of distribution — those established channels of distribution that adapt to the changing environment and revise their business model to service the new needs of the Smart Lighting customer. Moore said in his book:

“The final pieces of the strategy come into play across the chasm: distribution and pricing. Distribution is the vehicle that will carry us on our mission, and pricing is its fuel. These two issues are the only two points where marketing decisions come into direct contact with the new mainstream customer. The number-one corporate objective, when crossing the chasm, is to secure a channel into the mainstream market with which the pragmatist customer will be comfortable.”

That my friends is the new electrical/lighting distributor. I think we have crossed that big scary chasm (see the lower chart on the next page) in the Smart Lighting industry. Let me explain. First, wearing my academia hat, let me emphasize that markets are not products — they are people who buy those products, and those people have to be connected in order to be identified as a market. The Technology Adoption Life Cycle segments the high-tech market into the five categories shown in the lower image on the next page. In reading Moore’s book, I thought about how to apply his thinking to the Smart Lighting industry now emerging, and asked myself just how big the chasm is between the early markets and the mainstream markets.

The initial/early market for a disruptive technology is made up primarily of innovators and early adopters. We start the marketing process by understanding how these customers think, and more importantly why they buy. Only then can we re-position our business model and develop the marketing strategies to serve the new needs of our customers. The emphasis is on “the new needs.”

Innovators: The Techy Enthusiasts

1. They love and buy new technology for its own sake.

2. They will spend hours to make it work even when the product is not ready for prime time.

3. They make great critics because they truly care.

4. They’re gatekeepers — those competent enough to do the early evaluation.

5. Marketing must pay them heed. They will provide great feedback and will start to build support.

Small in numbers (2% to 5% of the market), the solid-state lighting (SSL) technology got complete buy-in from the Techy Enthusiasts. They love Smart Lighting because lighting is not just about illumination anymore. The techies evaluated and appreciated the superiority of the new high-tech lighting sources over their traditional alternatives.

Early Adopters:

The Visionaries

1. They are the “dreamers” who look to take quantum leaps forward.

2. They love disruptive innovation and are not looking for just improvements but breakthroughs.

3. Visionaries really drive the high-tech industries.

4. They alert the business community to pertinent technological advances.

5. Easy to sell but very hard to please, these dreamers always want more and can be unreasonable.

6. They love test pilot projects “to go where no man has gone before.”

7. They are highly demanding, impatient, see windows of opportunity as fleeting, and buy in early or not at all. For them, instant gratification is not fast enough anymore.

The market size for the Visionaries is estimated at 13% to 15%, so it’s significant and is a valuable source to court in the Smart Lighting market. I believe the industry is managing the expectations of the visionaries by working on not only LEDs but OLEDs, plasma, white lasers, nanowires, graphene, IoT, connectivity, Li-Fi, on and on. Visionaries are the ones who gave Smart Lighting our first big break. I think our industry is in the right place at the right time to take advantage of this opportunity. The dream is alive and doing rather well.

The market starts to unfold as it should when the techies connect with the visionaries. They start to foresee an order-of-magnitude leap in the innovation that they see as achievable. But we are talking about maybe at most 15% of the total available target market. Consumer acceptance, growth and business success can only happen when we cross the chasm into the mainstream majority markets of 65% to 70%. If that does not happen, we have nothing. Obviously, things get a lot more complex when we deal with the dynamics of the mainstream markets.

Early Majority:

The Pragmatists

1. Accepted as leaders by the late majority, who only follow when the early majority buys in.

2. The Pragmatists are not pioneers, they want the early market players to “debug” the high-tech product.

3. They look to make incremental, measurable, predictable progress.

4. They manage risk very closely and are receptive to case studies/testimonials to determine how others have fared.

5. Increased productivity drives their decisions but natural prudence and budget restrictions keep them cautious.

6. They are hard to win over but are very loyal once won.

7. New entrants have a hard time selling to Pragmatists because they communicate vertically (B2B), place high importance on references and relationships, and they want to buy from established businesses.

8. The good news for new entrants is once newcomers earn their way in, Pragmatists tend to be very loyal and even go out of their way to help start-ups succeed.

9. A few driving forces influence when Pragmatists continue to buy: standardization, product quality, support infrastructure, systems interfaces, reliability of service, relationships with value-added resellers (VARs). These all tend to depend on existing distribution relationships as a single point of control.

10. Must be convinced that once they make the decision to buy in, it’s for the long haul.

11. They love and encourage competition to keep costs down, provide alternatives, purge the market and establish proven market leaders.

Ok, where are we? We agree that consumer acceptance, growth and business success can only happen when we cross the chasm into the mainstream majority markets of 65% to 70%. If that does not happen, you have nothing. Now I’m not talking about the chasm between the early market and the laggards. That’s not a chasm — it’s a thermodynamic black hole. I have high school buddies who have a flip phone for emergency use only. Try telling them that only 10% of a phone is now used as a phone.

We have crossed the chasm. Here’s how I know:

- In 2011 LED lamps were 5% of the lamp market, but by 2014 they jumped to 30.7% of the market.

- In 2011 LED outdoor fixtures were 26% of the fixture market, and just three years later they had jumped to 54%;

- LED indoor fixtures jumped from 9% to 35% from 2011 to 2014.

As I mentioned earlier, understanding the mainstream market is complex and requires real marketing acumen. The Smart Lighting industry has many expert players in this field and what they are doing is working. The early majority is buying in in great numbers and my prognostication is that the majority (over 50%) of all lighting in all categories will be SSL by the end of next year. That means we are moving through the Total Adoption Life Cycle rapidly and we are reaching the late majority now.

Late Majority:

The Conservatives

1. Conservatives are a hard sell because they just do not like discontinuous innovation. Once they find something that works for them, they want to stick to it. High-tech products cause them angst.

2. They want to stay on par with the rest of the world but tend to get stung by the new technologies. Unfortunately, they have a hard time understanding how high-tech products work and the result is they do not work for them, at least initially.

3. They like to wait until sheer volume of sales encourages discounted prices.

4. Comfort level is most important to Conservatives.

5. After-purchase service is extremely critical to encourage continuing loyalty even if they are unwilling to pay for this service.

6. They rely, even depend, on strong distribution channels to provide a “product systems solution” to help them upgrade to something too daunting to handle by themselves.

7. Conservatives greatly extend the market for high-tech products that are no longer state-of-the-art.

8. You know you are in the mature stage of a product life cycle when the Conservatives buy-in in great numbers.

The LED outdoor lighting fixture market is already here. Just look at the many cities upgrading their street lighting to LEDs; all the sports arenas with new LED systems; and the bridges, roadways, landscape, security, area lighting applications all lit by LEDs. The Laggards and my high school buddies will be the only ones left standing. Conservatives are very cautious, and as we see, don’t like change very much but as prices continue to be cost competitive, they will join the parade and be very happy they did.

This is where I come down on my debate with Chris “Chicken Little” Brown of Wiedenbach Brown. Disintermediation will never happen. If we agree on the thinking and buying habits of both mainstream majority markets (70% in total), manufacturers don’t want to serve the late majority directly for sure and the early majority poses too many needs they are just not equipped to serve.

Manufacturers should focus on the Innovators and Early Adopters to continue to innovate and make the most advanced high-tech products possible. Fortuity is being in the right place at the right time and the established distribution channels are in the best position to continue to serve the mainstream markets for lighting. It is too important a product category to abandon. Don’t just sit there, make something happen!

Bill Attardi has been in the lighting business for more than 50 years. Now publisher of the energywatchnews.com blog, his first full-time job after three years in Army security was as a sales rep for Westinghouse Lamp in New York. Humble beginnings led to executive posts with Westinghouse, Philips, USI Lighting and a position as part owner in Wellmade Products. In 1994 he founded Attardi Marketing, a marketing and training company. He has an MBA in marketing and is an adjunct professor at Monmouth University and Brookdale Community College in N.J. You can reach him at [email protected].