We are now almost at the half way point of 2016 and it’s clear that industry sales will cross into negative territory for the year as a whole. As a matter of fact, industry sales were down more than 1.5% in the first quarter, and we view first quarter performance as history, not a forecast. But let’s try to put this in some context. Few if any industries can thrive against the tide of a slow-growing economy.

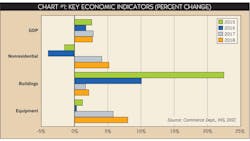

The economy has skidded along at a sub-par 2.5% rate over the past eight years. This is not meant to be a political comment but an observation that overall aggregate demand is performing less than the 3.5% long term growth of the overall economy. Aggregate demand performance hits the electrical industry through its direct impact on the crucial economic indicators that make this industry tick. In 2015, GDP was up 2.4%, while this year it is forecasted to advance a weak 1.7%, with the first quarter growth up just 0.5% from the year ago quarter. That’s the broad view.

Here are the pieces — the good news first. Regardless of weak aggregate demand, many distributors are seeing their sales up at high single and low double-digit rates. Here’s why. Take a look at a major subsector served by electrical distributors — nonresidential buildings. This subsector includes commercial, healthcare, shopping centers, strip malls and factory buildings. It’s part of the larger category of nonresidential construction.

Together, these expenditures are projected to increase 10% this year. In the first quarter these expenditures grew nearly 18%. That’s history. Is it any wonder that many electrical distributors had a very good first quarter? But in the next three quarters the combined growth of building construction will average less than 8%.

More good news. Residential spending is projected to grow a strong 9% this year after a nearly 9% increase last year.

Now the bad news. One key element of why the electrical industry behaves as it does is because nonresidential construction — a broad indicator of electrical industry performance — was negative to the tune of 1.5% last year, forecasted to decline 4% this year and was off nearly 4.5% in the first quarter of this year.

Let’s expand on this point. Some distributors can take it to the bank when some subsectors of the economy are expanding. But that does not drive the entire industry. It’s the combination of the broad indicators that drive it.

Falling output in the oil-producing areas has hit the electrical distribution industry hard. This sector is part of nonresidential construction and weighs down on growth substantially. With investment in mining and exploration off 35% last year and an expected decrease of 57% this year, overall investment in nonresidential construction fell 1.5% in 2015 and expected to decline about 4% this year.

What we are seeing is a divergence of the markets served by distributors. This is not unusual, but when the “right” factors come together it can spell trouble for the electrical distribution industry.

More bad news. Another key ingredient in the electrical industry mix is investment in business equipment. This indicator has a significant impact on distributor served industrial markets. Last year it was up just 1% followed by an expected gain of 0.2% this year. And of course distributor prices are falling at a rate of 3% this year after a decrease of 2.5% in 2015.

Bottom line is that the strength in the residential market is nowhere strong enough to offset the negatives in the other economic drivers. (See Chart 1, page 29.)

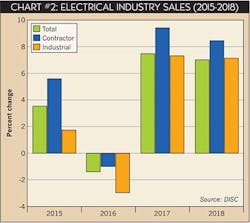

For 2017, we are projecting growth of about 7%. We see no negatives on the horizon as yet, after we work through this year. In addition, we expect industry sales to increase through 2018.

Notice in the sales chart on this page that the distributor-served contractor segment shows the greatest growth.

A forecast is only as good as how you apply it. This forecast like most forecasts only tells you about industry sales — the supply side of the industry. Your share measured against industry sales only addresses how well you are doing against your competitors. The supply side gives you insight on adding or reallocating resources. But it does not give you insight into how to grow your business or take share from your competitors.

In order to grow your business you need to know the demand side of the industry. The demand side tells you who is buying your products and how much they are buying. And it gives you the potential business that’s available to “take away” from your competitors.

Sizing your market by industries purchasing from distributors and applying industry and geographic multipliers is the only way you can begin to take share. It’s the demand side that gives you opportunities to grow your business. With a forecast of demand you can prospect for new business and compete in the demand arena for market share. But at the end of the day, the total supply and the total demand must be equal, and they are at the national level. However, the battles are always fought in the trading areas, and supply and demand are not always equal in these areas.

In 25 words or less, sales will be down 1.6% this year, up 7.3% next year and 7% in 2018. That’s what the model is saying as it tracks the key indicators of the electrical industry. In July we will update our numbers in line with how the economy is doing. Our forecast will take a hard look at industry sales this year and 2017-2018 as you move into the budget season this summer and fall.

About the Author

Herm Isenstein

Herm passed away in Sept. 2019 at the age of 86 from brain cancer. He was a good friend to the editors on the staff of Electrical Wholesaling and a prolific writer for the magazine for 15 years.

During his 30-plus years in the electrical industry, Herm Isenstein was the premier economist in the electrical wholesaling industry If you have any questions about DISC's subscription-based data services, contact Chris Sokoll, DISC's president at at 346-339-7528.